Market Commentary – October 2013

UK Summary

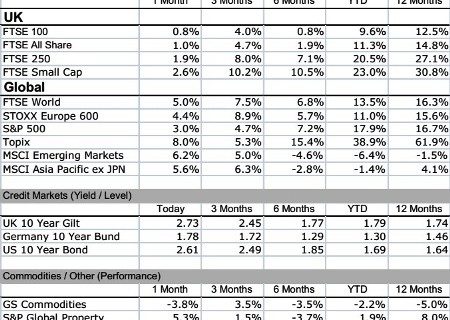

The UK macroeconomic picture continues to show improvement as the positive momentum started in the spring prevails with all three major economic sectors delivering encouraging readings. These readings, in conjunction with a slight reduction in unemployment, contributed a general “good feeling”. Once again we have noticed outperformance in equities that give exposure to the UK’s improving economic climate.

European Summary

European equities had a good month in terms of returns with the broad market index, Stoxx 600, returning 4.4%. Chancellor Merkel won the German election and now seeks to form a new coalition. Unemployment readings came in at 12.1% highlighting the structural issues in Europe with figures in Spain & Greece as much twice the average. The small economic improvements are encouraging but the equilibrium is still fragile, as the current Italian Government situation stands to prove.

US Summary

The big news of the month came from the US, where the FED decided not to change the asset purchase program. It also gave reassurance that the future tapering, which will take place, will not affect the portion allocated to mortgage backed securities. The official statement reiterated the current policy stand, that “more evidence of sustainable recovery and employment numbers are needed before any action is taken”. Clearly, markets reacted positively to this news. The end of the month was marked by the US Federal Government shutdown and once again the Debt Ceiling that is thought to be reached by October the 17th back to the fore.

Japan Summary

Japan had an exceptionally strong month returning 8%. The following weeks are critical for the country’s future development and precaution should prevail. Premier Abe will continue with the reform program by increasing as planed the sales tax in April 2014 from 5% to 8%.

Emerging Markets Summary

Emerging market central banks stepped in to support their currencies after QE tapering fears caused a sell-off earlier in the month. As “Operation Taper” was aborted BRIC equities returned in excess of 4% by the end of September